基本目标

Asset pricing: equity, bonds, derivatives

Asset allocation

Consumption timing

Financial engineering

AN INVESTMENT IS the current commitment of money or other resources in the expectation of reaping future benefits

These investment decisions are made in a competitive environment where

- higher returns usually can be obtained only at the price of greater risk

- it is rare to find assets that are so mispriced as to be obvious bargains.

Overview

- Financial assets

- Claims on real assets

- Stocks, bonds, mutual funds, bank deposits(银行存款), investment accounts(投资账户), and cash

- real assets generate net income to the economy

- financial assets simply define the allocation of income or wealth among investors

- 金融资产只是在投资者之间进行分配

- Financial assets are aggregated out and the total balance sheet for a country contains only real assets

- 金融资产流动性更高

- 金融资产更难定价

金融市场和经济

- informational role

- 资金流向前景最好的公司

- 与股价相关

- 投资时间

- 通过securities将消费推迟到下个周期

- 分散风险

- select securities consistent with their tastes for risk

- the firms that need to raise capital as security can be sold for the best possible price

- Separation of Ownership and Management

Mechanisms to mitigate agency problems:

- Tie managers’ income to the success of the firm (stock options)

- Monitoring from the board of directors

- Monitoring from the large outside investors and security analysts

- Takeover threat

Investment Process

composition

- Portfolios

- Asset classes

- stocks, bonds, real estate, commodities,…

- Asset Allocation

- The security selection

- Investment choice of which particular securities to hold within each asset class

- Security analysis: the valuation of particular securities

process

- “Top-down” approach

- 先从资源配置出发,再具体到证券或股票

- First step: Asset allocation

- Second step: security selection

- “Bottom-up” approach

- Investment based solely on security selection

- Disadvantage: may result in unintended heavy weight of a portfolio in only one or another sector of the economy

- Advantage: focus the portfolio on the assets that seem to offer the most attractive investment opportunities

Competitive Market

no “free lunches”

$\color{red}{\text{Risk-Return Trade-Off}}$

- If you want higher expected returns, you will have to pay a price by accepting higher risk

Diversification

- When we mix assets into diversified portfolios, we need to consider the interplay among assets and the effect of diversification on the risk of the entire portfolio\

有效市场假说

- In fully efficient markets when prices quickly adjust to all relevant information, there should be neither underpriced nor overpriced securities

Passive Management(被动投资)

- 接受市场大盘

- Holding a highly diversified portfolio(分散投资)

- No attempt to find undervalued securities

- No attempt to time the market

Active Management(主动投资)

- Finding mispriced securities(选股)

- Timing the market(择时)

Players

- Demanders of capital – Firms(企业部门)

- Net borrowers of fund: raise capital to pay for investments in plant and equipment

- income generated by those real assets provides the returns to investors who purchase the securities issued by the firm.

- Suppliers of capital – Households(住户部门)

- Net suppliers of capital: purchase the securities issued by firms

- Governments (政府)

- Can be both borrowers or lenders

Financial Intermediaries:

- to bring the suppliers of capital (investors) together with the demanders of capital

- Pool and invest funds the primary social function is to channel household savings to the business sector

Players

- Commercial Banks

- Investment Companies

- Mutual funds (共同基金)

- pool and manage the money of many investors, who are assigned a prorated(按比例分配) share of the total funds according to the size of their investment

- economies of scale (由规模经济决定)

- large-scale trading and portfolio management

- for small investors

- Trust

- design portfolios specifically for large investors with particular goals.

- Investment Bank

- Advice on how to price new securities (stocks ,bonds)

- Sell newly issued securities to public in the primary market

- Investors trade previously issued securities among themselves in the secondary markets

- venture capital (VC, 风险投资)

- Investments in Start-up companies: invest in them in return for an ownership stake in the firm

- Source: venture capital funds, wealthy individuals known as angel investors, and institutions such as pension funds

- Venture capital investors commonly take an active role in the management of a start-up firm

- Private equity(PE)

- also invest in distressed firms, or merger & acquisition for restructuring firms

- Mutual funds (共同基金)

- Insurance companies

- Credit unions

Asset Classes and Financial Instruments

Money Market (货币市场)

- Money market assets

- short-term debt, liquid, low risk

- Classification by market participants:

- Interbank market (银行间市场, wholesale)

- Participated by banks, non-bank financial institutions and large corporations

- Interbank market (银行间市场, wholesale)

- Money market mutual funds (货币基金)

- allow individuals to access the money market

- Higher interest rate than bank deposit

- Risk-free rate for individual

Money Market securities

- Treasury Bills: 政府发的短期债券

- Certificates of deposit(CD)

- Time deposit with a bank (定期存款)

- CDs issued in denominations greater than $100,000 are usually negotiable ( can be sold to another investor)

- Short-term CDs (maturity lower than 3month) are highly marketable

- Eurodollars(欧洲美元)

- Dollar-denominated time deposits in banks outside the U.S.

- Commercial paper(商业票据)

- unsecured debt of a company

- Short term (1-3 months)

- Considered to be safe because a firm’s financial condition is predictable in short term

- Bankers’ Acceptances(银行承兑汇票)

- An order to pay a bank on a future date by a bank’s customer

- For international trade financing (国际贸易工具)

- Repurchase agreement or Repo(回购)

- 见 #固定收益证券分析

- Issuer of repo sells government securities to an investor, with an agreement at a slightly higher price

- The increase in the price is the interest

- Usually overnight

- Short-term loans in interbank market backed by government securities

- Reverse repo (逆回购)

- The buyer of repo, investor

- Interbank loans(银行间同业拆借)

- Fed funds(联邦基金): Very short-term loans between banks in US

- The LIBOR Market(伦敦银行同业拆放利率市场)

- LIBOR rate

- LIBOR stands for London Interbank Offer Rate

- a rate charged in an interbank lending market outside of the U.S. (largely centered in London)

- typically quoted for 3-month loans

- Except for Treasury bills, money market securities are not free of default risk

- TED stands for Treasury–LIBOR spread

- credit spread for banks

- LIBOR rate

Bond Market

$\color{red}{详见固定收益证券分析}$

- Treasury Notes and Bonds(中长期国债)

- Inflation-Protected Treasury Bonds

- TIPS

- Inflation-Protected Treasury Bonds

- Federal Agency Debt(联邦机构债券or政策性债)

- 政策性金融机构债:国家开发银行(后改为开发性金融机构)、中国农业发展银行、进出口银行

- International Bonds

- Municipal Bonds(市政债券)

- Corporate Bonds(公司债券)

- Mortgages and Mortgage-Backed Securities(按揭与按揭支持证券)

Equity Securities

- Common stock(普通股or股票): Ownership

- Residual claim

- Limited liability

- Preferred stock(优先股): Perpetuity

- Fixed dividends

- Priority over common

- Tax treatment

- American Depository Receipts(美国存托凭证)

- Certificates traded in U.S. markets that represent ownership in shares of a foreign company(如百度、新 浪、搜狐等在美国上市的中国公司)

- CDR(Chinese Depository Receipt)

Stock Market Indexes

- Dow Jones

- Includes 30 large blue-chip corporations

- Computed since 1896

- Price-weighted average

- Standard & Poor’s 500

- Broadly based index of 500 firms

- Market-value-weighted index

- Others

- NYSE Composite

- NASDAQ Composite

- Wilshire 5000

Chinese Index

- 上证综指(全样本、市值加权)

- 深证综指(全样本、市值加权)

- 沪深300(流动性强、市值大、流通市值加权)

- 中证500(剔除沪深300、流动性和市值排序、流通市值加权)

Derivative Market

A derivative (证券衍生品or衍生品) is a security that gets its value from the values of another asset, such as commodity prices, bond and stock prices, or market index values.

- Options(期权)

- Call(看涨期权): Right to buy underlying asset at the strike or exercise price(执行价)

- Value of calls decreases as strike price increases

- Put(看跌期权): Right to sell underlying asset at the strike or exercise price

- Value of puts increase with strike price

- Value of both calls and puts increases with time until expiration

- 有价格

- 权利而非义务

- Call(看涨期权): Right to buy underlying asset at the strike or exercise price(执行价)

- Futures Contracts(期货合约)

- An agreement made today regarding the delivery of an asset (or in some cases, its cash value) at a specified delivery or maturity date for an agreed- upon price, called the futures price, to be paid at contract maturity

- Long position(买方): Take delivery at maturity

- Short position(卖方): Make delivery at maturity

- 必须执行交易

Basics of Investing Mechanism

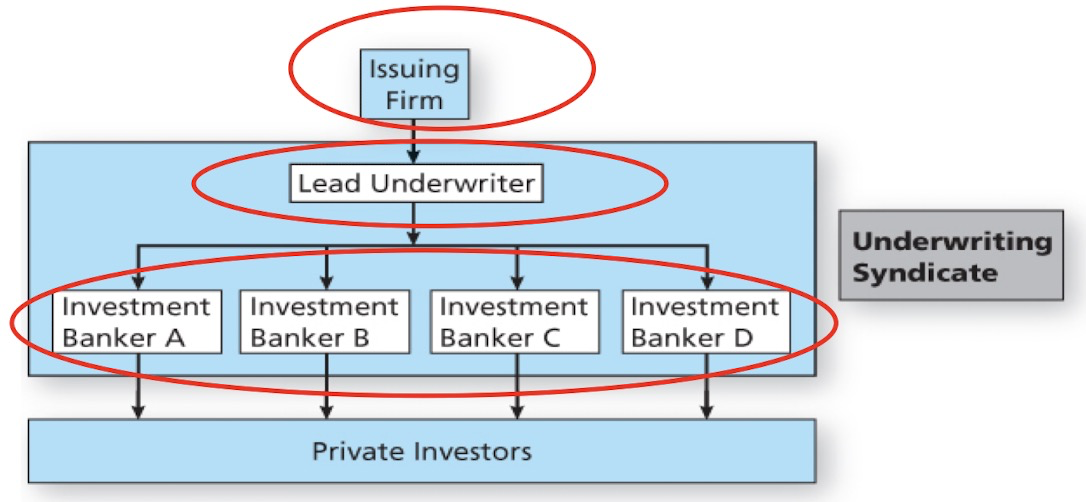

How Firms Issue Securities

- Primary Market

- Market for newly-issued securities

- Firms issue new securities through underwriter (investment banker) to public

- Secondary Market

- Investors trade previously issued securities among themselves

- Companies

- Privately Held Firms

- Up to 499 shareholders

- Raise funds through private placement

- Lower liquidity of shares

- Have fewer obligations to release financial statements and other information

- Publicly Traded Companies

- Raise capital from a wider range of investors through initial public offering, IPO

- Seasoned equity offering: The sale of additional shares in firms that already are publicly traded

- Public offerings are marketed by investment bankers or underwriters

- Registration must be filed with the Security regulators (eg SEC, CSRC)

- Raise capital from a wider range of investors through initial public offering, IPO

- Privately Held Firms

中国股票发行制度及改革

- 审批制(examination and approval,1991-2000)

- 采用行政和计划的办法分配股票发行的指标和额度

- 核准制(approval, 2001-2020)

- 取消了指标和额度管理

- 证券中介机构:发行是否符合市场条件

- 证券监管机构:发行是否符合监管条件

- 注册制(registration, 2020-)

- 市场化发行制度:发行公司股票的规模和定价由市场判断

- 注册制注重信息披露:对申报文件的全面性、准确性、真实性和及时性作形式审查

- 23年,全面注册制

IPO, initial public offering

- (under registration system)

- File prospectus to security regulator

- Road shows to publicize new offering

- Determine demand for the new issue (Bookbuilding)

- Degree of investor interest in the new offering provides valuable pricing information

- Underwriter bears price risk associated with placement of securities:

- IPOs are commonly underpriced compared to the price they could be marketed (IPO discount)

- Some IPOs are well overpriced others cannot even fully be sold

How securities are traded

- Types of Markets:

- Direct search

- Buyers and sellers seek each other

- Brokered markets

- Brokers search out buyers and sellers

- Dealer markets

- Dealers have inventories of assets from which they buy and sell

- 注意broker和dealer的区别

- Bid-ask spread is the profit for a dealer

- Auction markets

- Traders converge at one place to trade

- Direct search

- Types of Orders

- Market orders

- 直接交易,按照市场价

- Price-contingent Order

- Traders specify buying or selling price

- 包括:Limit-Buy Order, Stop-Buy Order, Limit-Sell Order, Stop-Loss Order

- Market orders

Trading Mechanisms

Dealer markets

Electronic communication networks (ECNs)

- True trading systems that can automatically execute orders

Specialists markets

- Maintain a “fair and orderly market”

- Have been largely replaced by ECNs

New trading strategies

- Algorithmic Trading

- The use of computer programs to make trading decisions

- High-Frequency Trading

- Special class of algorithmic with very short order execution time

- Dark Pools

- Trading venues that preserve anonymity, mainly relevant in block trading

- Algorithmic Trading

Bond Trading

- Most bond trading takes place in the OTC market among bond dealers

- NYSE Bonds is the largest centralized bond market of any U.S. exchange

- Market for many bond issues is “thin” and is subject to liquidity risk

Trading Costs

- Brokerage Commission:

- Fee paid to broker for making the transaction

- Explicit cost of trading

- Spread: Difference between the bid and asked prices

- Implicit cost of trading

- the price concession an investor may be forced to make for trading in quantities greater than those associated with the posted bid or ask price

- 例如,买一50手,卖一30手,卖二20手,不能只买卖一的。

Brokerage account

- Cash account 现金账户

- A brokerage account in which all transactions are made on a strictly cash basis.

- Margin account 信用账户(融资融券)

- A brokerage account in which securities can be bought and sold on credit.

Margin(保证金)

- The portion of the value of an investment that is not borrowed in a margin purchase

- Margin rate = Equity/Value of investment

- The portion that is borrowed incurs an interest

- This interest is set by brokers

- determined by the rate brokers pay to borrow money plus a service charge charge

- Initial Margin 初始保证金

- the minimum margin requirement when you first purchase securities on margin

- Currently 50% for stocks; you can borrow up to 50% of the stock value

- Maintenance Margin 维持保证金

- the minimum margin that you must need to maintain in a margin account after your initial purchase.

- Margin Call

- When the margin drops below the maintenance margin, the broker issues a margin call.

- It requires the investor to bring the margin back up to an acceptable level (most of the time the initial margin level)

- add new cash or securities, pay off the loan, or sell enough current securities

- If investors do not act, the broker has the right to sell securities from the account.

- Margin is a Financial Leverage

- the impact is to magnify both your gains and your losses

Short sale

After short sales, the investor have a short position

an investor who buys and owns shares of stock is said to be long in the stock or to have a long position.

For short position, sell high buy low

For long position, buy low sell high

Risks

- Long position in stocks:

- Upside return (unlimited)

- Downside losses (limited: -100%)

- Short selling stocks:

- Upside return (limited: +100%)

- 股价最低到0,而且几乎不可能达到

- Downside losses (unlimited)

- 股价升值

- Upside return (limited: +100%)

- Long position in stocks:

Short sale mechanisms

- Proceeds from the short sale must be kept on account with the broker

- the short seller does not earn interest on the short proceeds and cannot use the proceeds for another transaction

- If any dividends are paid on the stock while you have a short position, you must pay them.

- 分红必须返还

- A short position can be covered at any time before the securities are due to be returned.

- At any time, the security lender may call for the return of his shares

- The security borrower (short seller) must buy shares on the market and return them to the lender (or he must borrow the shares from elsewhere).

- 只要lender想要,必须返还

Short Sqeeze 挤兑

- A short squeeze

- heavily shorted security moves sharply higher, forcing short sellers to close out their short positions and adding to the upward pressure on the stock.

- 知道卖空的人多,故意抬高价格

- Short sellers are being squeezed out of their short positions

Impact of short selling on financial market

- Pros

- Enhance the liquidity and efficiency of the market.

- Help security price discovery: exploits market mistakes about firms’ fundamentals. Curb “pump and dump”.

- Uncover fraudulent accounting and other problems at companies

- Cons

- Abusive short selling can be used for market manipulation:

- aggressively driving down a stock price through heavy short selling, then buying the shares for a large profit

- Lead to the undesired market volatility

- Abusive short selling can be used for market manipulation:

Short selling for investors

- Pros

- Some investors are better at identifying overpriced, bad companies than underpriced, good companies.

- 相当于long position的反向

- Many institutions won’t do short selling, leaving unexploited short selling opportunities from which you can benefit.

- Hedging. A portfolio including both long and short positions in stocks which tend to move together will generally have lower volatility than one which has only long positions.

- 对冲风险

- Some investors are better at identifying overpriced, bad companies than underpriced, good companies.

- Cons

- There’s unlimited downside potential and limited upside potential.

- You’re fighting the trend of the market, which is, in the long run, up.

- Money from a short sale is used as collateral for the owner of the borrowed shares. You aren’t earning interest on the proceeds from short sales.

- You have to pay any dividends that are earned.

- Another company could acquire the company you’re shorting, at a significant premium, thus driving up the share price.

- Sometimes shares aren’t available to short.

- The obligation to buy and return the shares whenever the lender call for the return of his shares

Risk and Return

Interest rate

- Equilibrium real rates are determined by demand for funds supply and demand of funds

- The supply of funds from Households

- The demand for funds from Businesses

- Government can provide either net supply of or demand for funds

- 就是 #经济学原理 里面的供给需求线的交汇

- Equilibrium nominal rate

- investors should be concerned with real returns

- When expected inflation rate is higher, nominal interest rates should be higher

- This higher nominal rate is necessary to maintain the expected real return offered by an investment

- Fisher’s hypothesis

- Nominal rate should increase one-for-one with increases in the expected inflation rate

- $$r_{nom}=r_{real}+E(i)$$

- difficult to test the hypothesis because the equilibrium real rate also changes unpredictably over time

some returns

- APR: auunal percentage return

- simple compounding

- T < 1 year

- $$APR=r_f(T)\times (1/T)$$

- EAR: effective annual return

- T > 1 year

- $$1+EAR=[1+r_f(T)]^{1/T}$$

- HPR: holding period return

- $$HPR=\frac{P_1-P_0+D_1}{P_0}$$

excess return

- Excess return: the difference between the actual rate of return on a risky asset and the actual risk-free rate

- Risk premium is the expected value of the excess return, 是期望

- Risk is measured by standard deviation

- Risk aversion

- The degree to which investors are willing to commit funds to stocks

Time series analysis

Estimated Expected Return through historical data

- $$E(r)=\sum_{s=1}^Np(s)r(s)=\frac{1}{N}\sum_{s=1}^Nr(s)$$

- 把每个数据点等价加权

- If the time series of historical returns fairly represents the true underlying probability distribution, then the arithmetic average return from a historical period provides a forecast of the investment’s expected future HPR

The arithmetic average provides an unbiased estimate of the expected future return.

Geometric (Time-Weighted) Average

- $$g=TV^{1/n}-1, \text{where } TV_n=(1+r_1)(1+r_2)…(1+r_n)$$

- $TV_n$ is the Terminal value of the investment

几何平均总小于算术平均

- For normal distribution: $E(\text{Geometric average})=E(\text{Arithmetric average})-\sigma^2/2$

Using historical data with n observations, we could estimate variance is

- $$\hat{\sigma}^2=\frac{1}{n}\sum_{s=1}^n[r(s)-\bar{r}]^2$$

historical performance measure: geometric

Forecast: arithmetic

Sharpe ratio

investments typically entail accepting some risk in return for the more excess return

- If we are willing to face risk, then we can expect to earn a risk premium

- the trade-off between reward and risk

$$\color{red}{\text{Sharpe ratio}=\frac{\text{Risk premium}}{\text{SD of excess return}}}$$

- 通常来说,high risk high return

Risk Aversion and Capital Allocation to Risky Assets

speculation vs. gamble

- speculation (投机)

- Taking considerable risk for a commensurate gain

- Reject a fair game

- Only accept risk for risk premium

- Speculators are Rational

- Taking considerable risk for a commensurate gain

- gamble (赌博)

- Bet on an uncertain outcome for enjoyment

- Accept a fair game or a negative value game

- Do not requires risk premium for taking risks

- Gamblers are irrational, subject to behavioral bias

- Bet on an uncertain outcome for enjoyment

risk aversion and utility

- Risk-averse Investors are speculators in capital markets

- Investors invest in portfolios of assets

- reject investment portfolios that are fair games or worse

- Risk aversion measures investor’s preference for risk

- Different investors are different in risk aversion

- assess the risk aversion level of an investor by his utility score

- Risk averse investors are willing to consider:

- Risk-free assets

- Speculative investments with positive risk premiums

- Risk tolerance: inverse of risk aversion

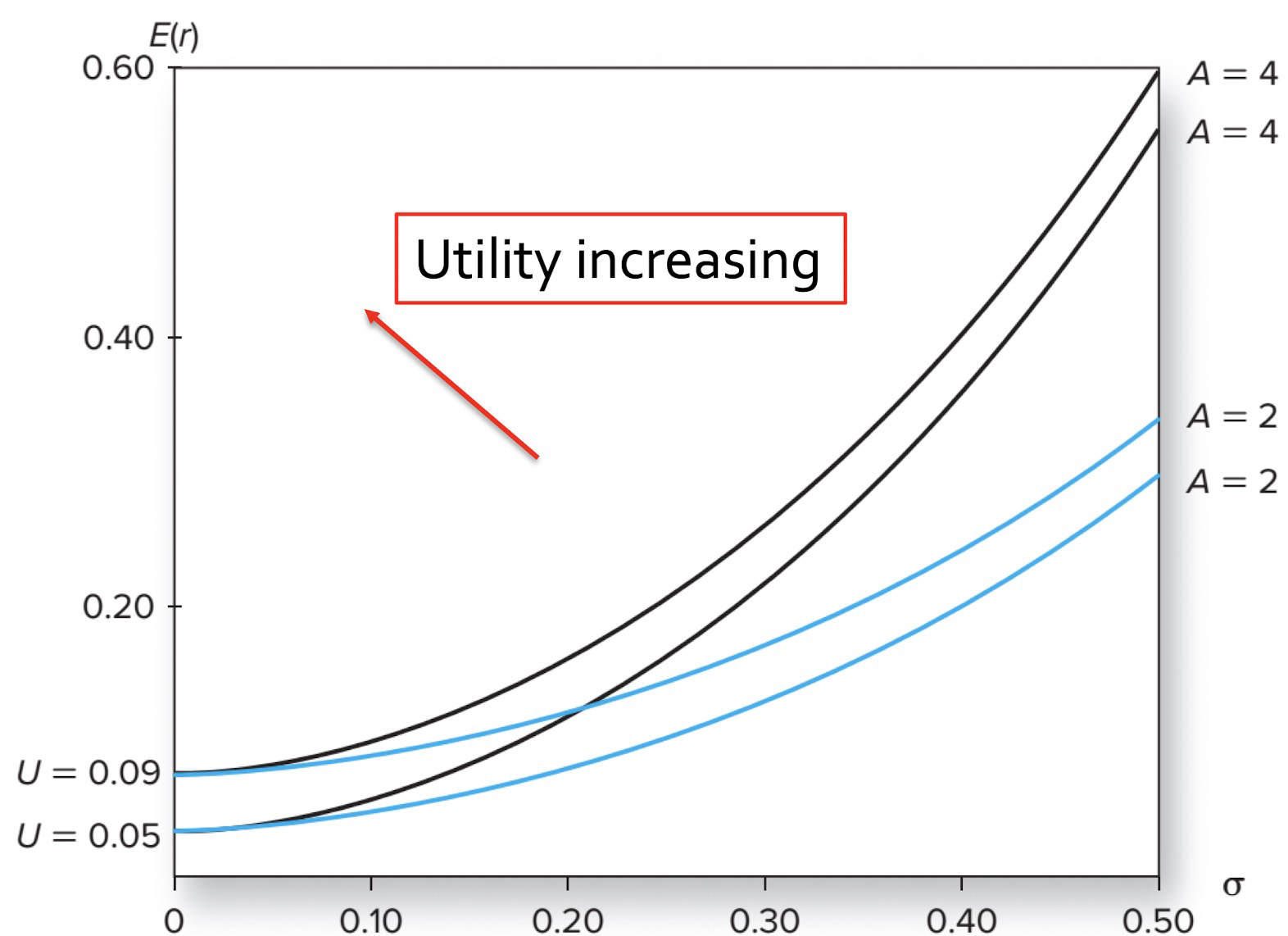

Mean variance utility

- A = coefficient of risk aversion

- $$U=E(r)-\frac{A}{2}\sigma^2$$

- Risk averse investor: A>0

- Risk neutral investor: A=0

- Risk lover investor (gambler) A<0

Certainty equivalent rate, CER

- 确定等价收益

- the rate that a risk-free investment an investor requires to provide the same utility as the risky investment

- An investment can be desirable only if its certainty equivalent return exceeds that of the risk-free

- The difference is the risk premium

Indifference curve

- An investor’s own indifference curves do not intersect

- Indifference curves of two investors might intersect

- Indifference curves have positive slopes

- In a set of indifference curves, the highest offers the greatest utility

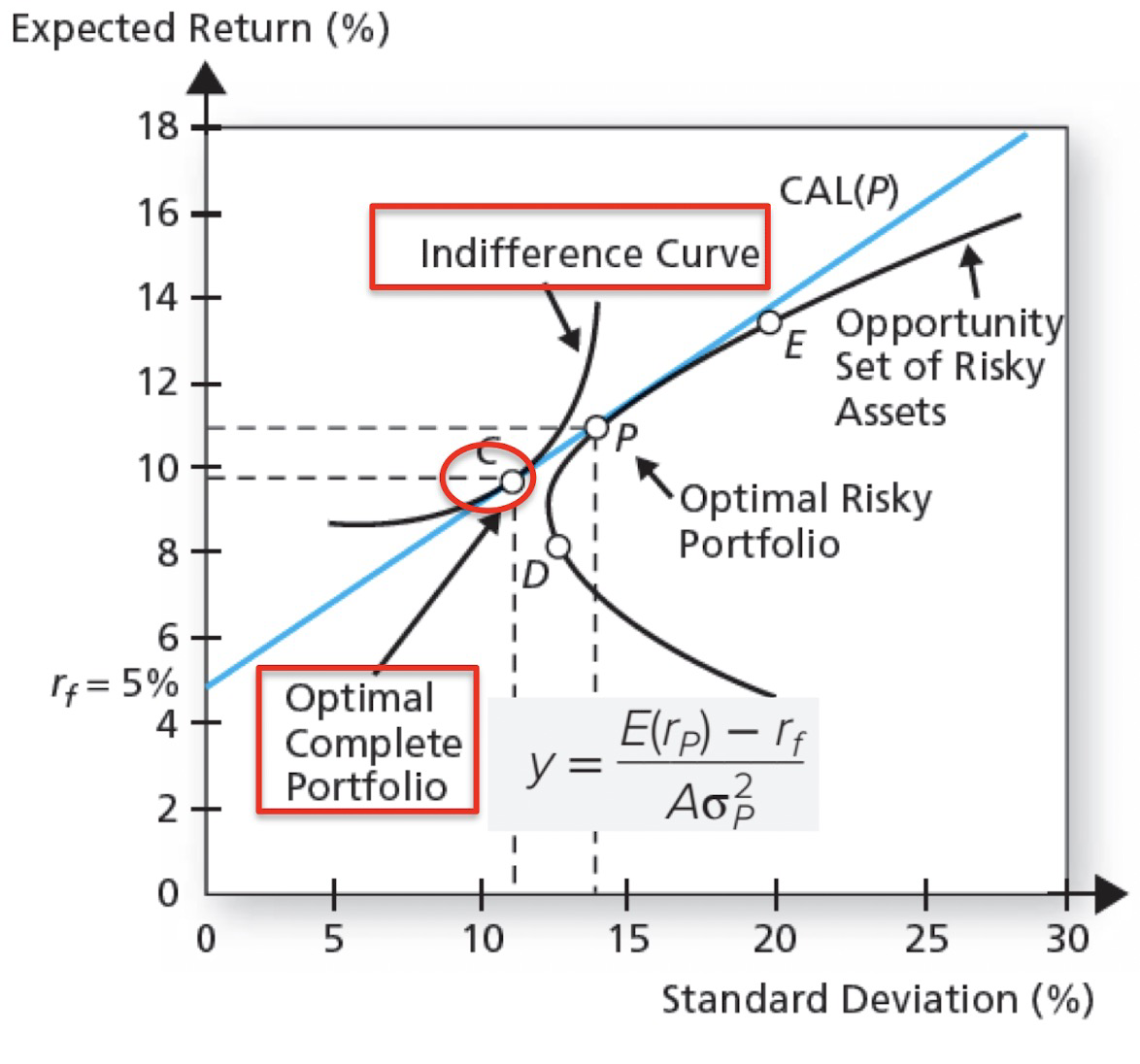

Capital Allocation

- The choice among broad asset classes : stocks, bonds, cash

- The most fundamental decision in investments

- The simplest way to control risk is to manipulate the fraction of the portfolio invested in risk-free assets versus in the risky assets

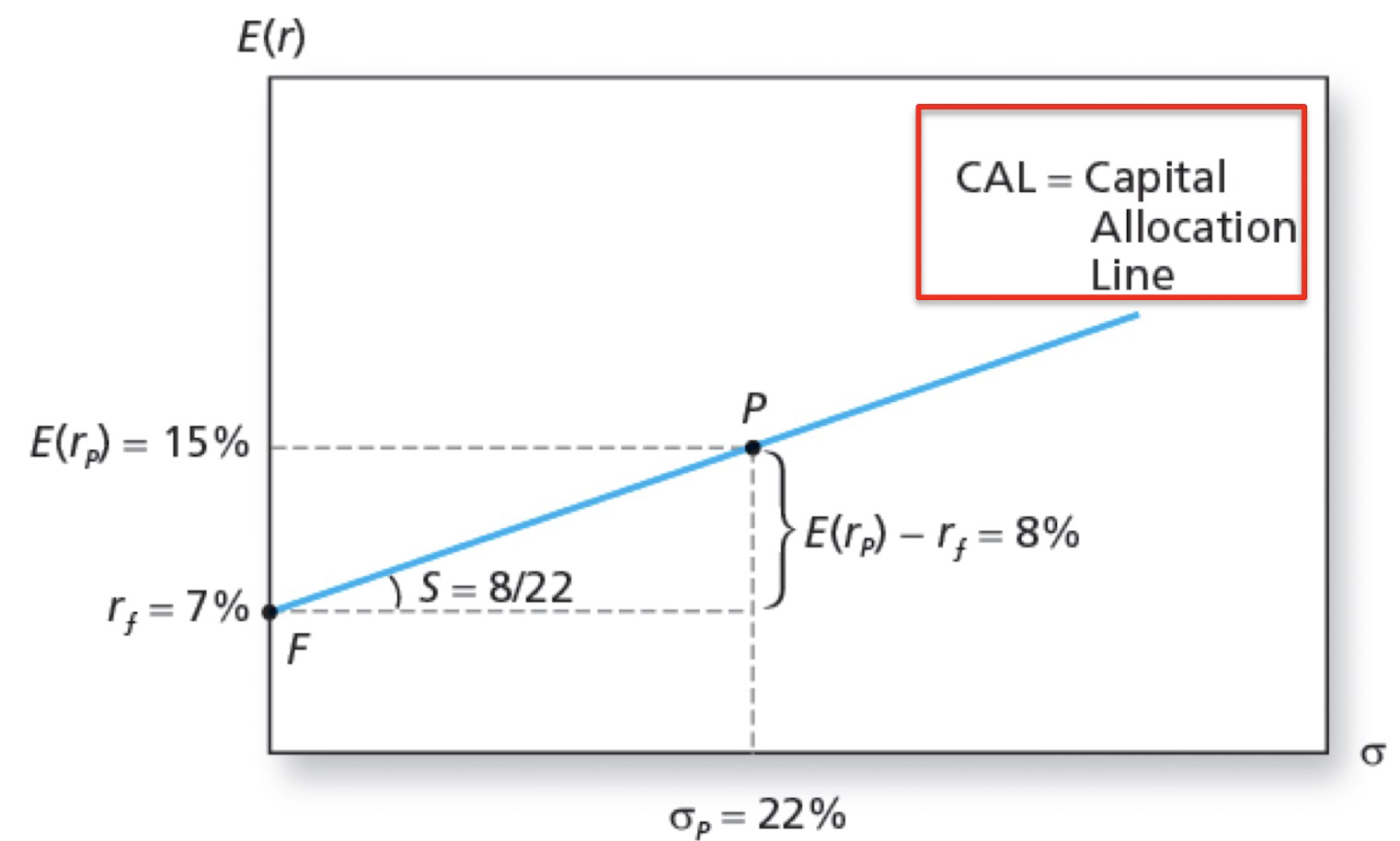

Capital Allocation Line (CAL)

- Investment opportunity set formed with a risky asset and a risk-free asset

- 只有一个risky asset和risk-free asset之间

- invertors 在这条线与Utility的切线点可以达到效用最大化

- optimal position in risky:

- $$\color{red}{y^*=\frac{E(r_p)-r_f}{A\sigma_p^2}}$$

Passive strategies

- The passive strategy avoids any direct or indirect security analysis

- Supply and demand forces may make such a strategy a reasonable choice for many investors

- A natural candidate for a passively held risky asset would be a well-diversified portfolio of common stocks such as the S&P 500

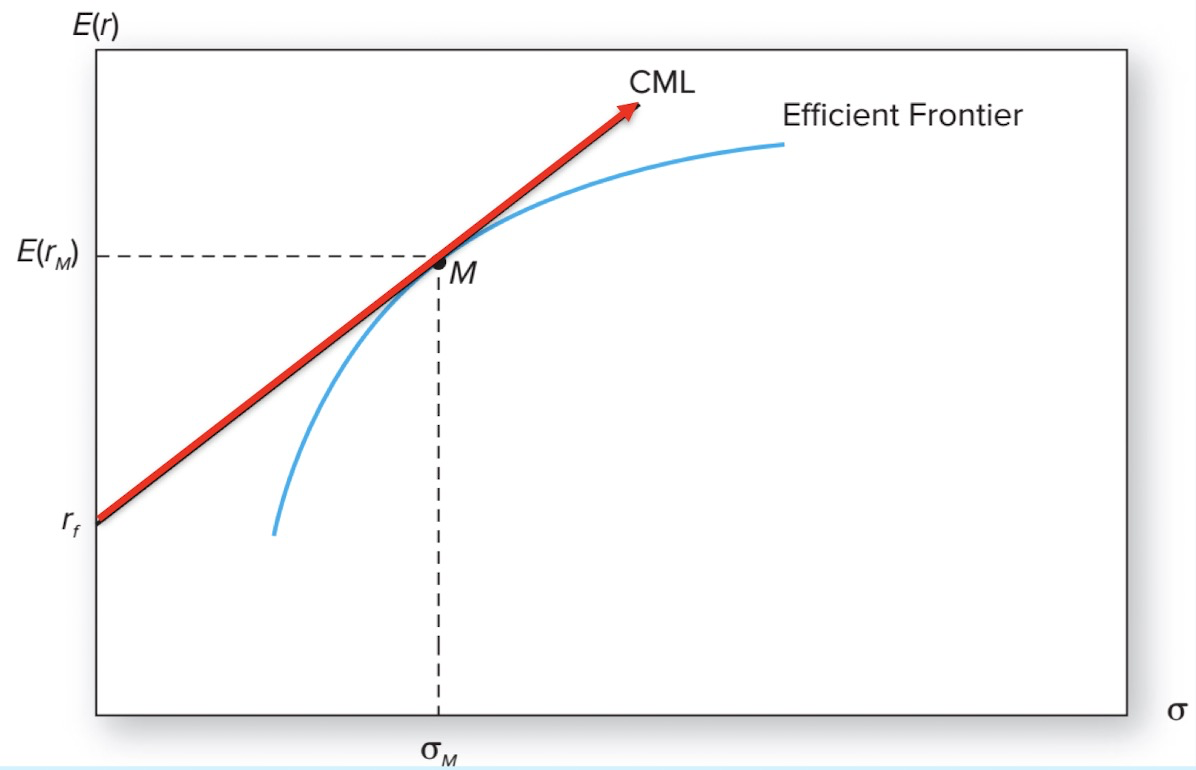

Capital Market Line, CML

- a capital allocation line formed investment in two passive portfolios

- Virtually risk-free short-term T-bills (or a money market fund)

- Fund of common stocks that mimics a broad market index

- 是由risk-free asset与market index连线

MPT and CAPM

Diversification

portfolio可以分散公司的自有风险,不能分散公司的系统性风险

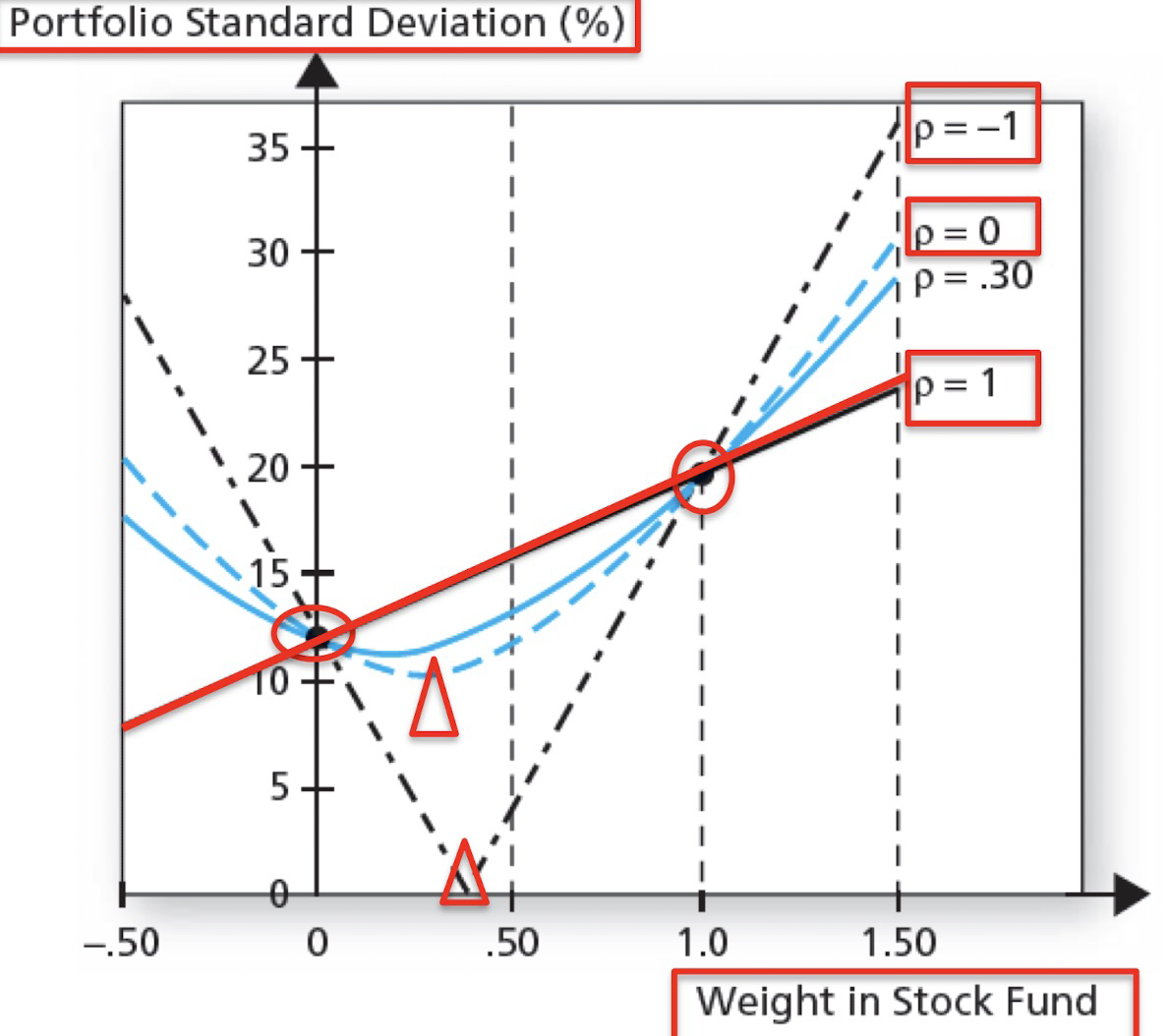

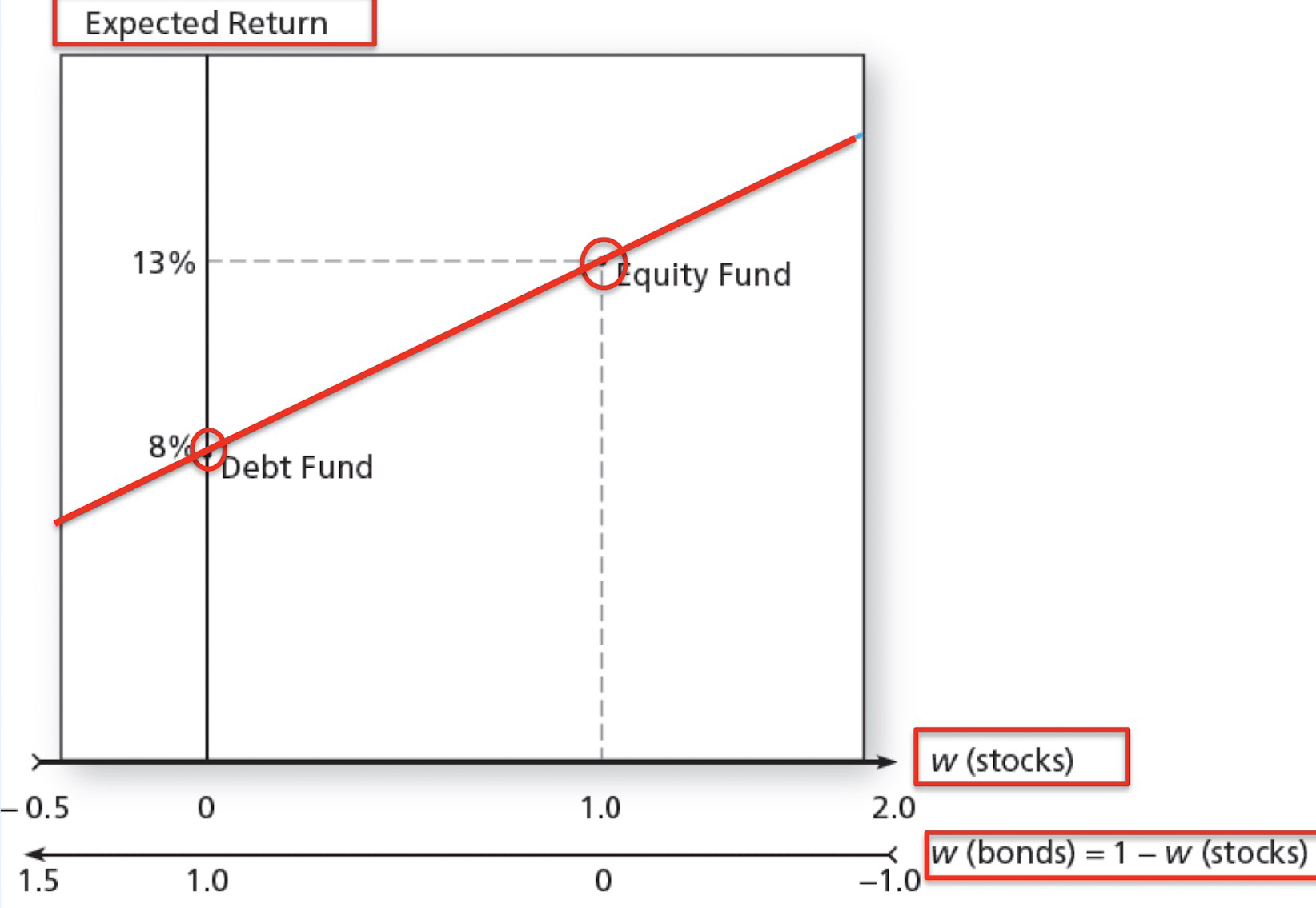

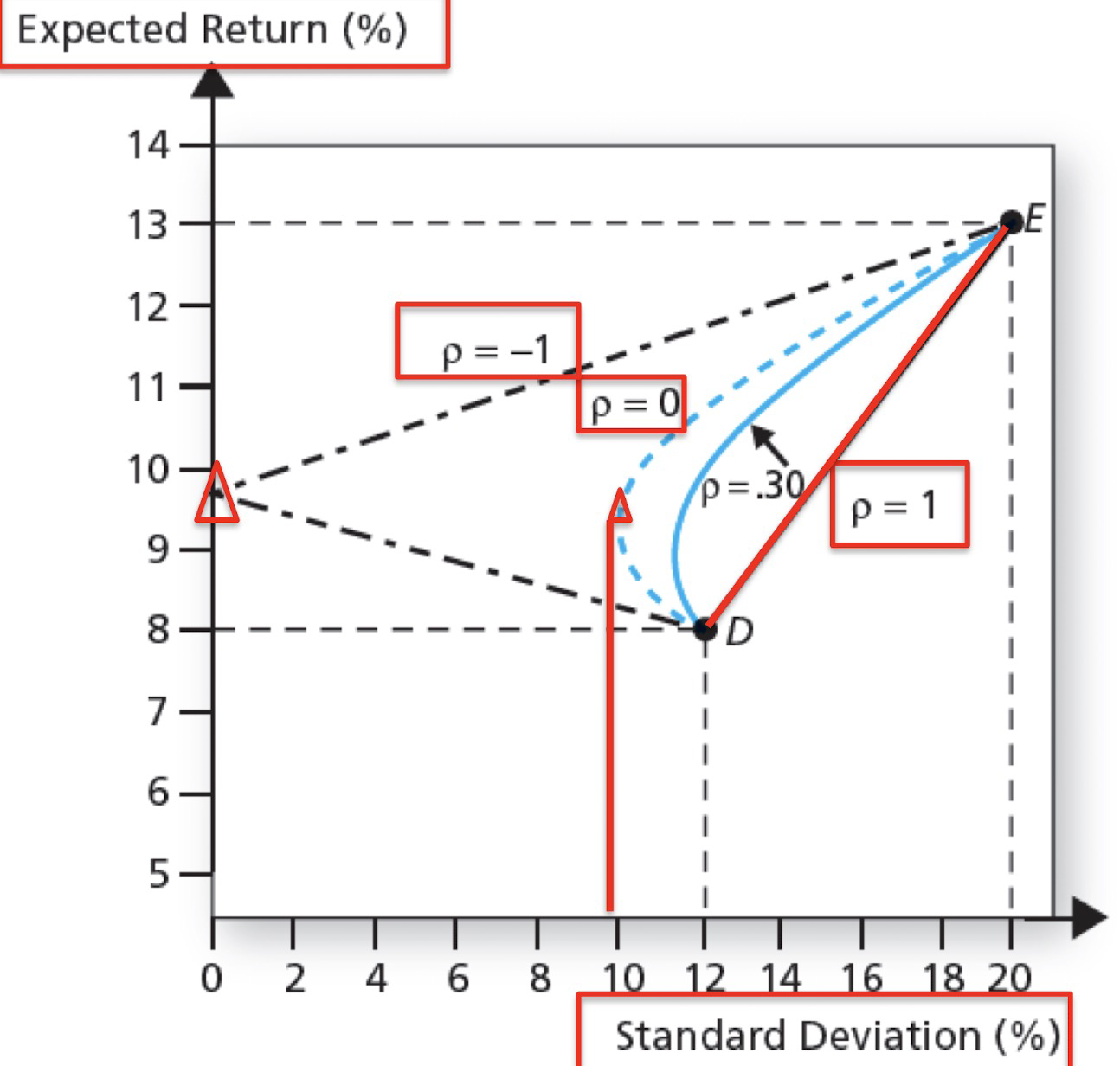

Portfolio of two risky assets

- 假设是debt和equity

- Portfolio return $$E(r)=w_DE(r_D)+w_EE(r_E)$$

- Portfolio Variance $$\sigma_p^2=w_D^2\sigma_D^2+w_E^2\sigma_E^2+2w_Dw_ECov(r_D,r_E)$$

- $$Cov(r_D,r_E)=\rho_{DE}\sigma_D\sigma_E$$

- 当相关系数为1时,没有任何风险被分散

- 当相关系数为-1时,可能构造出一个风险为0的组合,完全对冲风险

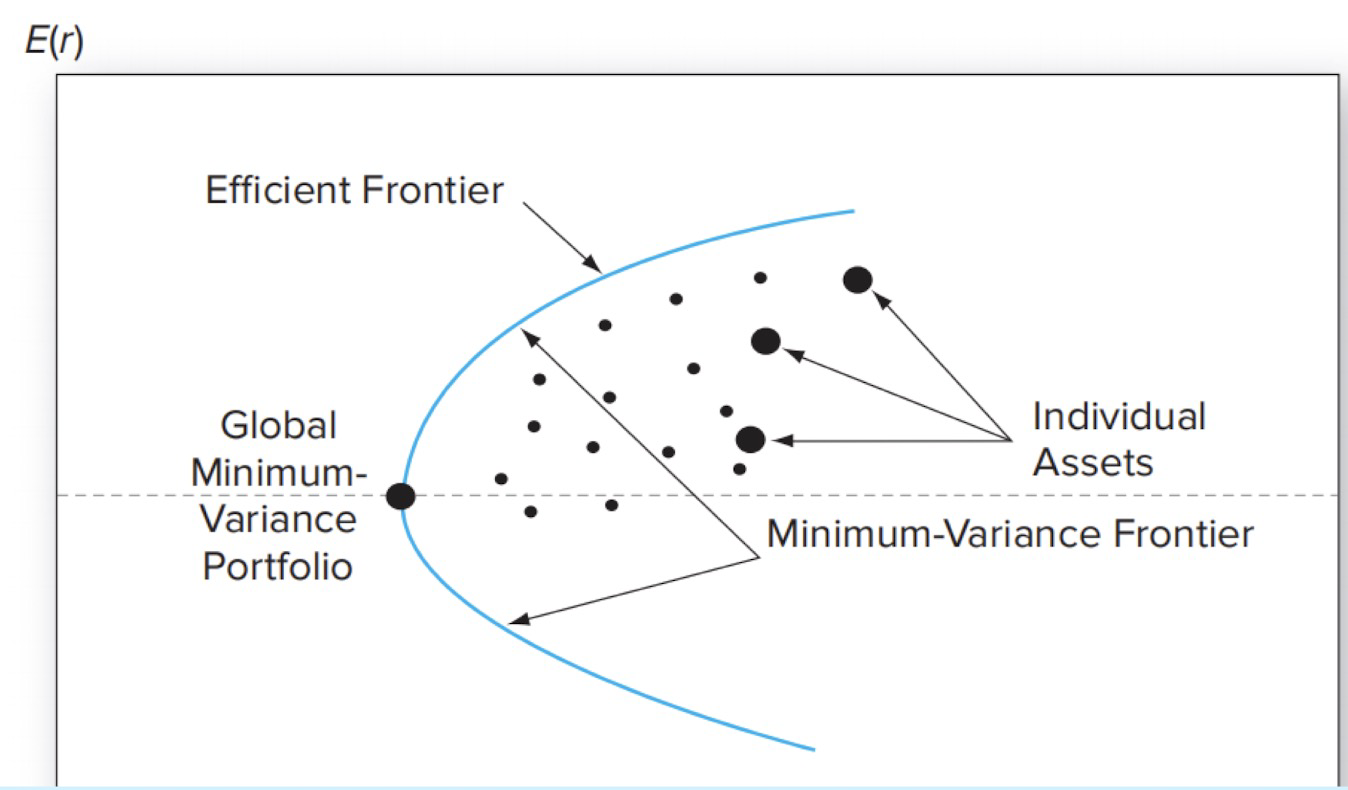

Global Minimum Variance Portfolio (MVP)

- The minimum variance portfolio is the portfolio composed of the risky assets that has the smallest standard deviation; the portfolio with least risk

- 当相关系数>0时,不可能减小风险

- 当相关系数=0时,总风险可能比两个分别都小

- 当相关系数<0时,可能构造出risk-free

portfolio return and variance

- 这条线是Opportunity Set of risky assets

Determination of the optimal overall portfolio

- Optimal portfolio selection for N risky assets and one risk free asset:

- Efficient frontier: identify the risk–return combinations available from the set of risky assets

- 找到所有risky asset组成的组合的可能性边界,不考虑risk-free asset

- Security selection: Determination of the optimal risky portfolio

- 找Sharpe ratio最大的点,也就是切点

- Capital allocation: Allocation of the complete portfolio to risk-free versus the risky portfolio depends on personal preference

- 在这条切线上找与Utility相切点

- Efficient frontier: identify the risk–return combinations available from the set of risky assets

Markowitz Portfolio Optimization Model

Method 1

- $$\sigma_p^2=\sum_{i=1}^N\sum_{j=1}^Nw_iw_jCov(r_i,r_j)$$

- $$min_{w_i}\sigma_p^2 \quad\text{, so that } \quad E(r_p)=\sum_{i=1}^Nw_ir_i=R$$

Method 2

- $$max_{w_i}S_p=\frac{E(r_p)-r_f}{\sigma_p} \quad \text{subject to } \quad \sum w_i=1$$

CAL: introduce the risk-free asset

Separation Principle

- Everyone invests in P, regardless of their degree of risk aversion

- More risk averse investors put more in the risk-free asset

Assumptions

- Investor behavior

- Investors are rational, mean-variance optimizers.

- Their investment horizon is a single period

- Investors use identical input list for efficient frontier (homogeneous expectation)

- Market structure

- All assets are publicly held and trade on public exchanges

- Investors can borrow or lend at a common risk-free rate, and they can take short positions on traded securities

- No taxes

- No transaction costs

Market portfolio

Equilibrium Conditions

Each investor’s risky portfolio holding is

- $$y=\frac{E(r_m)-r_f}{A\sigma_m^2}$$

We aggregate all investors together, In equilibrium, all borrowing and lending cancelled

- Assume average investor’s risk averse $\bar{A}$

- y = 1

- thus, $E(R_m)=\bar{A}\sigma_m^2$

portfolio risk

- $$\sigma_p^2=\sum_{i=1}^n\sum_{j=1}^nw_iw_jCov(r_i,r_j)$$

market portfolio risk:

- $$\sigma_p^2=\sum_{i=1}^Nw_iCov(r_i,\sum_{j=1}^Nw_jr_j)$$

- $$\sigma_m^2=\sum_{i=1}^Nw_iCov(r_i,r_m)$$

- 每只stock对整体风险的贡献是这只股票与市场的Cov,不是自己的Variance

$$\frac{E(r_m)-r_f}{\sigma_m^2}=\frac{E(r_i)-r_f}{Cov(r_i,r_m)}$$

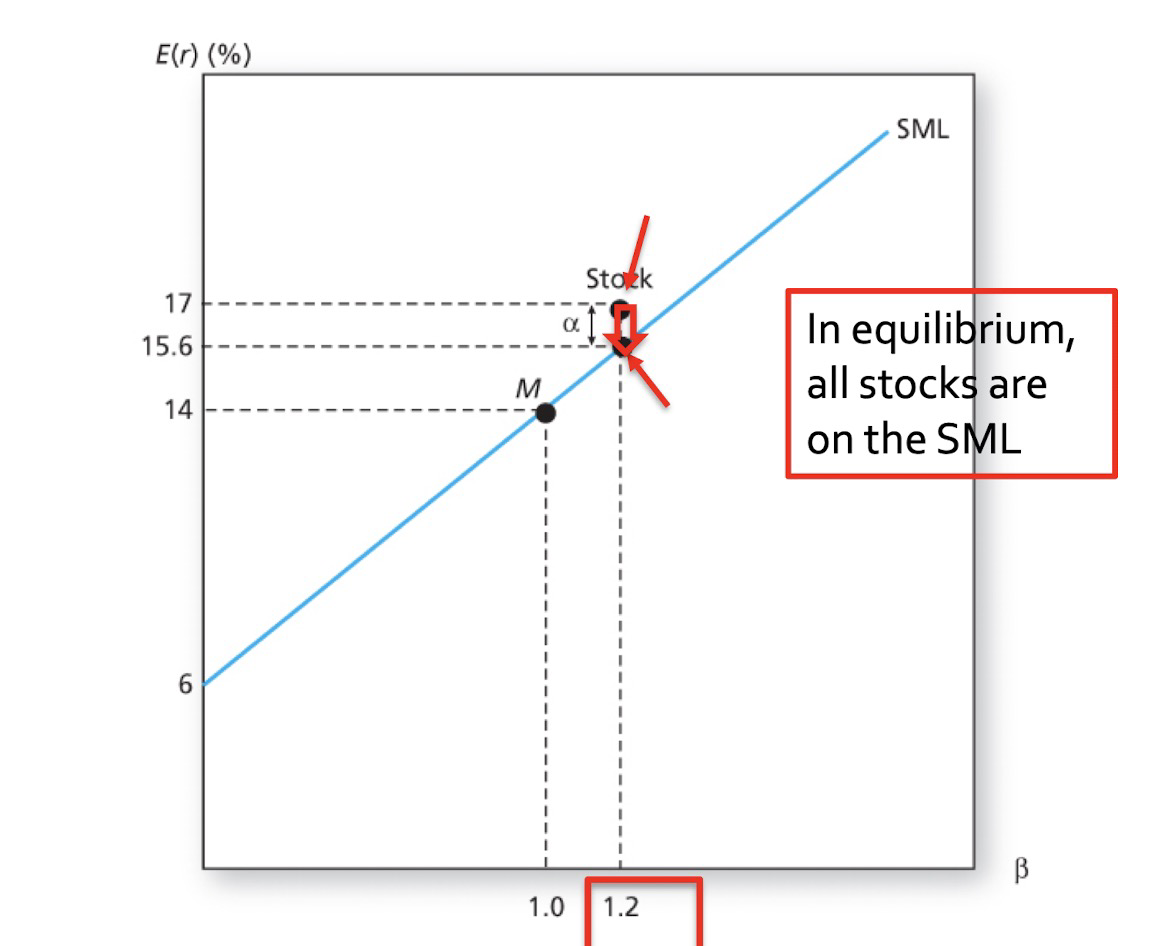

$$\text{Since }\beta_i=\frac{Cov(r_i,r_m)}{\sigma_m^2}\text{ , thus }\quad \color{red}{E(r_i)-r_f=\beta_i(E(r_m)-r_f)}$$

this is CAPM.

Security Market Line, SML

CAPM Application and Limitation

- CAPM holds for the overall portfolio

- Application: Provide a benchmark model for risk premium

- Application in corporate finance

- Cost of capital

- IPO pricing

- Limitation: CAPM only accounts for market risk

- Systematic risk other than market risk such as Non-tradable risk, Liquidity risk, inflation, interest rate …

Index Model

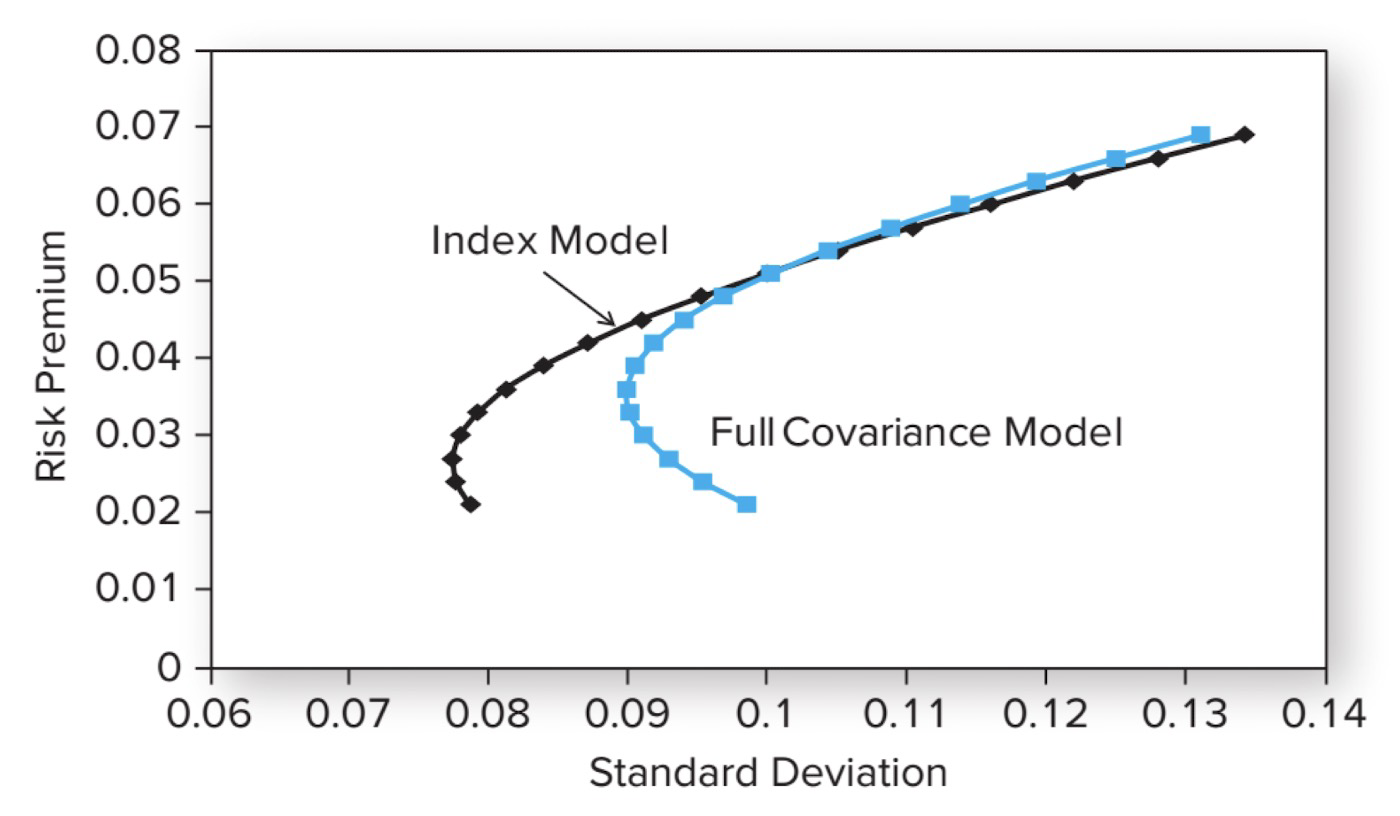

Problems with Markovitz model

- The covariance matrix is too large to be estimated accurately

- For example, the covariance of n=50 stocks consists of $(n^2 –n)/2=1325$ estimations

- Inconsistent estimation of correlation matrix

- The covariance matrix is too large to be estimated accurately

Factor Model

- The actual rate of return on any security

- $r_i=E(r_i)+\text{unanticipated surprise}$

- The actual rate of return on any security

Single factor model

- Single factor model: decompose risk (the unanticipated surprise) into

- A systematic risk factor (denoted as m)

- Firm specific risk(denoted as $e_i$)

- Covariance between stocks are due to their covariance with systematic risk factor m

- $$\color{red}{r_i=E(r_i)+\beta_im+e_i}$$

- $$E(m)=0,E(e_i)=0$$

- m 和 $e_i$ 是独立的

- $E(r_i)$ 无方差

- $\beta_i$, the sensitivity for firm i

- the total variance of $r_i$ is

- $$\sigma_i^2=\beta_i^2\sigma_m^2+\sigma^2(e_i)$$

- Cov between two firm’s return is

- $$Cov(r_i,r_j)=Cov(\beta_im+e_i,\beta_jm+e_j)=\beta_i\beta_j\sigma_m^2$$

- 当n很大时,firm-specific risk被消去了,只剩系统风险

single index model

When single factor is a market index (or generally well-diversified portfolio)

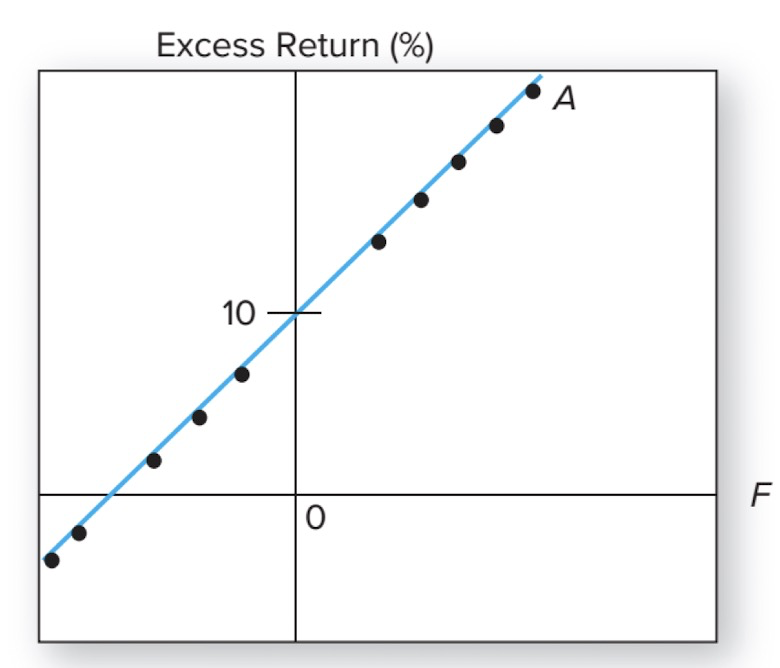

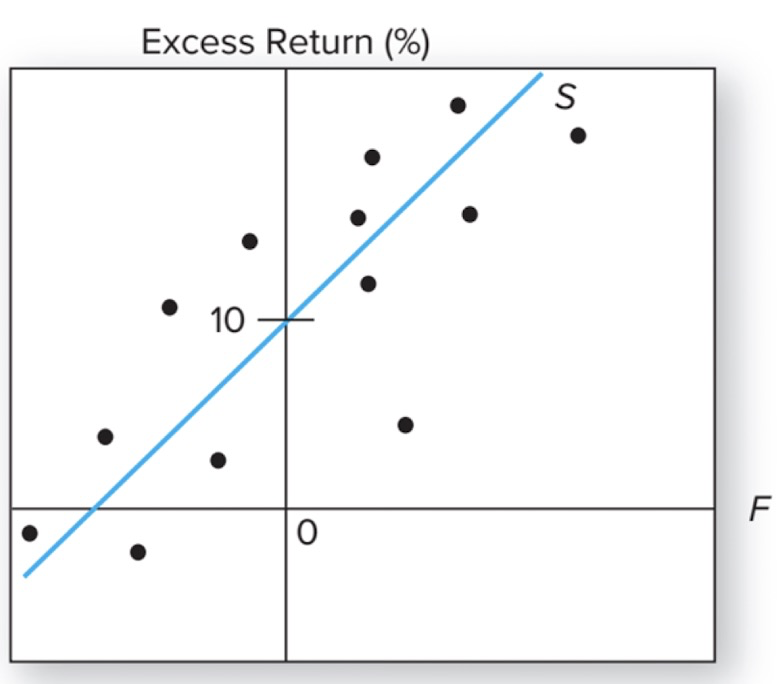

Security characteristic line

- $$R_i(t)=\alpha_i+\beta_iR_m(t)+e_i$$

Expected Return–Beta Relationship

- $$E(R_i)=\alpha_i+\beta_iE(R_m)$$

- $$\color{red}{R-square=\frac{\beta_i^2\sigma_m^2}{\beta_i^2\sigma_m^2+\sigma^2(e_i)}}$$

Single index model: a framework that separates macroeconomic and security analysis

- Macroeconomic analysis : estimate the risk premium and risk of the market index.

- Statistical analysis : estimate the beta coefficients of all securities and their residual variances, $\sigma^2(e_i)$.

- Asset pricing model: The portfolio manager uses the estimates for the market-index risk premium and the beta coefficient of a security to establish the expected return of that security

- Security analysis: expected return forecasts (alphas) are derived from various security-valuation models

Alpha

- Alpha(α) is a nonmarket premium (abnormal return)

- Depends on factor model

- α may be large if you think a security is underpriced and therefore offers an attractive expected return

- CAPM (or other competitive equilibrium model) predicts α will be zero

- Security analysis: each security analyst comes up with his or her own estimates of alpha

- A portfolio manager who has no special information about a security nor insight unavailable to the general public will take the security’s alpha value as zero

- alpha is the key variable that tells us whether a security is a good or a bad buy

- A positive-alpha security is a bargain and therefore should be over-weighted

The Industry Version of the Index Model

- Adjusted beta

- $\text{Adjusted beta}=\frac{2}{3}\text{estimated beta}+\frac{1}{3}$

- Why adjusted beta

- empirically, beta coefficients seem to move toward 1 over time

- statistically, the average beta over all securities is 1. Before estimating the beta of a security, our best forecast would be that it is 1.

- Predicting beta

- One simple approach would be to collect data on beta in different periods and then estimate a regression equation

- $\text{current beta}=a+b\times (\text{past beta})$

- Different predicting variables

- $\text{current beta}=a+b_1\times (\text{past beta})+b_2\times (\text{firm size})+b_3\times (\text{debt ratio})$

- One simple approach would be to collect data on beta in different periods and then estimate a regression equation

Portfolio construction and the single index model

- A simple way to achieve diversification: include the S&P 500 index portfolio as one of the assets of the portfolio

- Passive portfolio: If no security, portfolio manager(PM) would hold the S&P 500 as a passive portfolio

- It gives broad market exposure without the need for expensive security analysis

- Active portfolio: With security analysis, the PM may be able to devise an active portfolio that can be mixed with the index to provide a better risk–return trade-off

- Under single index model, the optimal portfolio can be derived explicitly, consisting of

- an active portfolio(A) comprised of the n analyzed securities

- the market index portfolio, the (n + 1)th asset (passive portfolio ,M)

构造方法

- 计算各个股票的权重为 $w_i^0=\alpha_i/\sigma^2(e_i)$

- 归一化 $w_i=w_i^0/(\sum w_i^0)$

- 计算active portfolio的α $\alpha_A=\sum w_i\alpha_i$

- 计算active portfolio的残差 $\sigma^2(e_A)=\sum w_i^2\sigma^2(e_i)$

- 计算active portfolio的初始权重 $w_A^0=(\alpha_A/\sigma^2(e^A))/(E(R_M)/\sigma^2M)$

- 计算active portfolio的beta $\beta_A=\sum w_i\beta_i$

- 调整初始权重 $w_A^*=w_A^0/(1+(1-\beta_A)w_A^0)$

- 组合的权重为 $w_M^*=1-w_A^\quad w_i^=w_A^*w_i$

相关数据:

- $$E(R_p)=(w_M^*+w_A^\beta_A)E(R_M)+w_A^\alpha_A$$

- $$\sigma^2_P=(w_M^*+w_A^\beta_A)^2\sigma_M^2+(w_A^\sigma(e_A))^2$$

- $$\color{red}{S_p^2=S_M^2+(\frac{\alpha_A}{\sigma(e_A)})^2}$$

- 其中 $(\frac{\alpha_A}{\sigma(e_A)})^2$ 是 information rato

- measures the extra return we can obtain from security analysis compared to the firm-specific risk

- the information ratio if optimized, is always increasing with increasing number of active security

- if a security’s alpha is negative, the security will assume a short position in the optimal risky portfolio

The index portfolio is an efficient portfolio only if all alpha values are zero from security analysis

CAPM, Multifactor model and APT

Single factor model

- $$R_i=E(R_i)+\beta_iF+e_i$$

- $R_i$ is excess return on security

- $F$ is Surprise in macro-economic factor

- F could be positive or negative but has expected value of zero

- $\beta_i$ Factor sensitivity or factor loading or factor beta

- $e_i$ Firm specific events (zero expected value)

index model and CAPM

- CAPM indicates $\alpha_i$ is 0

- $E(R_i)=\beta_iE(R_m)$

- assets should be on the security market line (SML)

CAPM

- The assumptions of the CAPM

- Single period investment (vs intertemporal risk premium fluctuation)

- investors face the same opportunity set

- No frictions

- All assets are traded: no untradable asset risk

- All investors are rational mean-variance optimizers with homogeneous expectations

- Systematic Risk beyond CAPM

- Inflation risk

- Uncertainty due to inflation rate

- Interest rate risk (Real)

- Volatility risk

- Liquidity risk

- Price risk due to transaction costs/trading friction

- Untradable asset risk

- labor income risk(unemployment risk)

- entrepreneurial risk

- housing price risk

- For long horizon investors, concerns about future risk premium changes over economic cycle

- Macro economic factors

- Inflation risk

Multifactor model

Possible common macro-economic factors

- Business cycle (GDP Growth)

- Interest Rates

- Inflation Rates

- Liquidity

Possible factors due to extra risk premium

- size

- Value

- Many firm characteristics seem to predict future returns (active current research area)

Example

- $$R_i=E(R_i)+\beta_{iGDP}GDP+\beta_{iIR}IR+e_i$$

- $$E(R_i)=\beta_{iGDP}RP_{GDP}+\beta_{iIR}RP_{IR}$$

- RP stands for risk premium

multifactor model

- Multiple risk exposures, each risk factor has its own risk premium

- Estimate a beta or factor loading for each factor using multiple regression

- $$R_it=\sum_{j=1}^k\beta_{ij}F_j+\epsilon_{it}$$

APT

- Multifactor version of security market line

- $$E(R_i)=\sum_{j=1}^k\beta_{ij}E(R_j^F)$$

well-diversified portfolio

- if a portfolio is well diversified, its firm-specific or nonfactor risk becomes negligible

APT(Arbitrage Pricing Theory)

The Law of One Price :

- if two assets are equivalent in all respects, they should have the same market price

Risk free arbitrage (a very strong assumption):

- any investor will want to take an infinite position in it

no-arbitrage condition:

- rules out the existence of arbitrage opportunities

In deriving APT, we assume risk-free arbitrage

Arbitrage pricing theory for any well-diversified portfolio:

$$\color{red}{E(r_i)=r_f+\beta_{i1}[E(r_1)-r_f]+\beta_{i2}[E(r_2)-r_f]}$$

Can be extended to multifactor model

if this equation is to be satisfied by all well-diversified portfolios, it must be satisfied by almost all individual securities

The Security Market Line of the APT

- Security market line for well-diversified portfolios

- $$E(R_P)=\beta_PE(R_F)$$

APT vs. CAPM

| APT | CAPM |

|---|---|

| Using any systematic risk factor | Model is based on an inherently unobservable “market” portfolio |

| Does not assume investors as mean-variance investors | rest on mean-variance efficiency. The actions of many small investors restore CAPM equilibrium |

| Apply to well-diversified portfolio | Apply to all assets |

Fama-French Three-Factor Model

- Size anomaly

- the market value of outstanding equity

- firms with small size outperforms large ones after accounting for CAPM market risk

- Value anomaly

- book value per share divided by stock price

- Firms with high book to market ratios outperforms lower ones

- Factors constructed based on the size and value anomaly

- SMB = Small Minus Big (firm size)

- HML = High Minus Low (book-to-market ratio)

- $$R_{it}=\alpha_i+\beta_{iSMB}SMB_t+\beta_{iHML}HML_t+\beta_{iM}R_{Mt}+e_{it}$$

- While SMB and HML are not themselves obvious candidates for relevant risk factors

- may proxy for hard-to-measure more fundamental variables

- firms with high book-to-market ratios are more likely to be in financial distress

- small stocks may be more sensitive to changes in business conditions

Efficient Market Hypothesis

- 1953年 Maurice Kendall 发现股价的波动时随机游走的。该怎么解释?

EMH

- Efficient Market

- Market prices reflect all relevant information at a given time

- New information is unpredictable

- if it could be predicted, then the prediction would be part of today’s information.

- Stock prices that change in response to new (unpredictable) information also must move unpredictably.

- Stock price should follow a random walk if market is efficient

- Efficient market ≠ perfect foresight market(无未知信息)

implication1

- EMH implies that there are no undervalued or overvalued financial assets

- A forecast about favorable future performance leads to favorable current performance, as market participants rush to trade on new information.

- Result: Prices change until expected returns are exactly commensurate with risk.

- the price is “right”

reasons

- 为什么市场是有效的

- driving force:competition and profit-motive

- 当基数很大时很小的 $\alpha$ 也能产生很高的收益

- 导致大基金公司倾向于寻找relevant information

- 为什么百分百有效不可能

- 只有当寻找信息的投入likely to 产生超额收益时才会愿意去投入时间和精力

- 在市场均衡时,有效的信息收集活动应当被奖励

- the degree of efficiency differs across various markets, depending on the information environment

Information Set for Market efficiency

- Strong-form efficiency: all information of any kind, public or private, are available

- Semistrong form efficiency: all publicly available information

- Weak form efficiency: past price and volume

EMH Implications 2

Technical analysis

- search for recurrent and predictable patterns in stock price

- Weak form efficiency implies technical analysis is useless

- Rationale

- a sluggish response of stock prices to fundamental supply and demand factors

- if the stock price responds slowly enough, the analyst will be able to identify a trend that can be exploited

Fundamental analysis

- using economic and accounting information to predict stock prices

- Study past earnings and balance sheets information

- detailed economic analysis (including the quality of the firm’s management, the firm’s standing within its industry, the prospects for the industry, etc)

- Semi-strong form EMH implies Fundamental Analysis is useless

Information analysis

- whether the information you obtained is already priced in the market?

- Whether the information source is trust worthy?

- How the information is processed?

inspiration

- try to find firms better than everyone’s estimates

- try to find poorly runned firms that are not that bad

Active and passive portfolios

- Active Management

- An expensive strategy

- Suitable only for very large portfolios

- Passive Management: No attempt to outsmart the market

- Accept EMH

- Index Funds and ETFs

- Very low costs

- 据统计,基金经理平均水平没有跑过大盘

Event study

- If security prices reflect all currently available information, then price changes must reflect new information

- 因此,measure the importance of an event by examining price changes during the period in which the event occurs

- Event study(短期事件分析)

- Method

- a technique to assess the impact of a particular event on a firm’s stock price

- If market is efficient, the event should not impact price before or after the announcement of the event

- Choose a time window (usually 10 days) around the event date to account for the information leakage and possible sluggish reactions

- Key issue: Isolating the part of a stock price movement that is attributable to a specific event

- Use of a “market model” to approximate for all other information impact on the stock return

- 也就是单因子模型寻找 $e_t$

- cumulative abnormal return (CAR), the sum of all abnormal returns over the time period

- application

- the Regulators use event studies to measure illicit gains captured by traders who may have violated insider trading or other securities laws

- Event studies are also used in fraud cases, where the courts must assess damages caused by a fraudulent activity.

- Method

Test EMH

statistical issues

- Magnitude Issue

- Only managers of large portfolios can earn enough trading profits to make the exploitation of minor mispricing worth the effort.

- Selection Bias Issue

- Only unsuccessful investment schemes are made public

- good schemes remain private.

- Lucky Event Issue

金融市场异常

- Anomaly is defined to be a deviation from a the CAPM (or other benchmark model)

- Return patterns that are unexplained by the CAPM are considered to be anomalous.

- Usually a significantly positive intercept (正的 $\alpha$)

Weak-form test (弱式检验)

- Returns over the Short Horizon

- Momentum

- Good or bad recent performance continues over short to intermediate time horizons

- Momentum

- Returns over Long Horizons

- negative long-term serial correlation in the stock return performance

- Behavioral explanation

- Episodes of overshooting followed by correction

- Overreaction leads to positive serial correlation (momentum) over short time horizons

- Subsequent correction of the overreaction leads to negative serial correlation over longer horizons

- stock price fluctuates around its fair value

Semistrong form test

- Size effect: small-firm effect

- higher average returns on small stocks than large stocks. Beta cannot explain the difference.

- Value effect: book-to-market ratios

- higher average returns on value stocks than growth stocks. Beta cannot explain the difference.

- Value firms: Firms with high B/M, E/P, D/P, B/P, or CF/P. The notion of value is that physical assets can be purchased at low market prices.

- Growth firms: Firms with low above ratios. The notion is that high price relative to fundamentals reflects uncapitalized growth opportunities, or real options

- Post-Earnings Announcement Price Drift

- earnings surprise

- Difference between actual earning and market expectations of earning

- Market expectations of earnings: measured by averaging the published earnings forecasts of analysts or by applying trend analysis to past earnings(一致预期)

- EMH suggets response to announcement should be quick

- For earnings announcement, positive (negative) surprise should lead to immediate positive (negative) stock returns

- Many studies find market price responses to earnings announcements are slow

- earnings surprise

Strong form test

- Inside Information

- 不会预期市场强有效,因为

- trading on inside information is illegal

- Security regulators (SEC or CSRC) require all insiders to register their trading activity

Explanations of anomalies

- rational explanations

- Fama French: explained by risk premiums

- Measuring abnormal performance: rely on a specific asset pricing model

- joint hypothesis problem: is it alpha or beta

- distinguish luck from skill

- Behavioral explanations

- evidence of inefficient markets

- irrational investors

Mutual fund performance

- The conventional performance benchmark today is a four-factor model, which employs:

- the three Fama-French factors

- the return on the market index, and returns to portfolios based on size and book-to-market ratio

- SMB,HML,$R_m-R_f$

- the three Fama-French factors

- plus a momentum factor (a portfolio constructed based on prior-year stock return)

Bonds

#见投资学与固定收益证券分析

一些要点:

- The bond price curve is convex

- The longer the maturity, the more sensitive the bond’s price to changes in market interest rates

- Current Yield

- Bond’s annual coupon payment divided by the bond price

- For premium bonds (bond price above par value)

- Coupon rate > Current yield > YTM

- Altman’s z-score model for bankruptcy prediction

- $$Z=3.1\frac{EBIT}{\text{Total Assets}}+1.0\frac{Sales}{Assets}+.42\frac{\text{Shareholders Equity}}{Total Liability}+ .85\frac{\text{Retained Earnings}}{\text{Total Assets}}+.72\frac{\text{Working Capital}}{\text{Total Assets}}$$

- Z < 1.23 , 有风险

- 1.23 < Z < 2.9 , 灰色区域

- Z > 2.9 , 安全

- Default yield spread

- The difference between the promised YTM and the expected YTM

yield curve

- Investors require a liquidity premium (or risk premium) to hold a longer-term bond

- $f_n$ generally exceeds $E(r_n)$

- The excess of $f_n$ over $E(r_n)$ is the liquidity premium (or term risk premium, or simply risk premium)

- The yield curve has an upward bias built into the long-term rates because of the risk premium

- An upward sloping curve could indicate:

- Rates are expected to rise (Expectation hypothesis)

- and/or

- Investors require large term risk premiums to hold long term bonds (liquidity preference/Risk premium theory)

- Inverted yield curve indicate that interest rates are expected to fall and signal a recession

Equity Valuation Models

感觉和 #公司金融 讲的又很像,简单写一下对照着看看吧。

Methods of Valuation

- Market value of equity: stock price too volatile

- Book values of equity: common shareholders equity

- based on historical cost

- It is possible, but uncommon, for market value to be less than book value.

- “Floor” or minimum value of the liquidation value per share

- Useful in bankruptcy

- Replacement value:

- Liquidation value, value through liquidation of firm’s assets

- Usually a measure for merger and acquisition

- Tobin’s q is the ratio of market price to replacement cost

- Intrinsic value: the present value of all cash payments to the investor in the stock, discounted at the appropriate risk-adjusted interest rate

- Dividend Discount Models (DDM)

- The growth rate in dividends (g) can be estimated in a number of ways

- Using the company’s historical average growth rate

- Using an industry median or average growth rate

- Using the sustainable growth rate.

- if a firm can generate return on investment (ROE) greater than its cost of capital, it will retain part or all earnings to sustain its growth

- $$g=ROE\times b$$

- The growth rate in dividends (g) can be estimated in a number of ways

- Free Cash Flow Models (useful for firms without stable dividend payments)

- Dividend Discount Models (DDM)

Price-Earning ratios and growth

- The value of the firm can be decomposed into two parts:

- the value of the assets already in place, the no-growth value of the firm

- Plus the NPV of its future investments, present value of growth opportunities

- $$P_0=\frac{E_1}{k}+PVGO$$

- $E_1$, earnings per share; k, required rate of return; PVGO, 未来预期增长机会现值

- The ratio of $PVGO/(E_1/k)$ is the ratio of firm value due to growth opportunities to value due to assets already in place

- Price-Earning ratio:

- $$\color{red}{\frac{P_0}{E_1}=\frac{1}{k}(1+\frac{PVGO}{E/k})}$$

- P/E rises dramatically with PVGO

- High P/E indicates that the firm has ample growth opportunities.

- 根据DDM, $P_0=\frac{D_1}{r-g}$, 则

- $$\frac{P_0}{E_1}=\frac{D_1/EPS}{k-g}=\frac{1-b}{k-ROE\times b}$$

- 当ROE、b增大时P-E增大

- 当风险变大时,k增加,P-E减小

记

这门投资学的课程内容含量确实不算高,金融课之间的许多知识点也是相通的,可以互相参考借鉴着学习并复习。